The Trump Account: Turning $1,000 Into a Long-Term Wealth Strategy

Most people will open this account and leave the most valuable part sitting on the table.

Here’s what’s easy to miss: Trump Account contributions are made after-tax. That creates a cost basis and cost basis opens the door to Roth conversions. Done at the right time, in the right amounts, this account can be gradually moved into a Roth IRA at little to no tax cost.

The window that matters most isn’t at birth. It’s from ages 18 through the early 30s — when many young adults have lower income, access to the standard deduction, and fewer competing tax obligations. That combination creates a rare opportunity to convert portions of the account each year, filling lower tax brackets intentionally, and shifting assets into tax-free territory over time.

And while you’re converting, the remainder keeps compounding. You’re not working through a fixed balance. You’re managing a growing asset — which is what turns a one-time tax decision into a long-term wealth-building system.

The timing, the sequencing, the interaction with other accounts is where the strategy lives. It’s also where most people need help.

So what exactly is a Trump Account?

Starting July 2026, children born between 2025 and 2028 are expected to receive a $1,000 government contribution into a new tax-advantaged investment account. Families can add up to $5,000 per year (indexed for inflation), employers can contribute up to $2,500 annually, and no earned income is required. Investments are limited to low-cost U.S. equity funds, and withdrawals are taxed as ordinary income unless, of course, you’ve planned around that.

On its own, it’s a decent head start. Paired with a conversion strategy, it’s something meaningfully different.

Why starting early changes everything

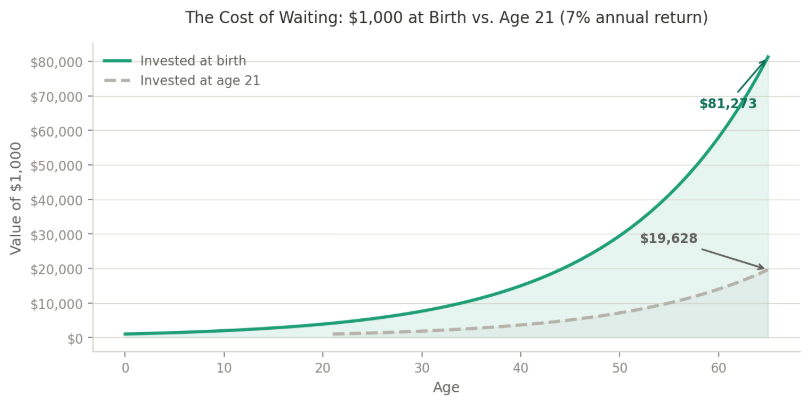

A $1,000 investment at birth, growing at 7% annually, reaches roughly $81,000 by age 65. The same $1,000 invested at age 21 reaches about $19,600 — less than a quarter as much. The account practically builds the case for itself.

Figure 1: $1,000 invested at birth vs. age 21 at a 7% annual return, through age 65.

Chart was generated using AI based on simple interest compounding calculator. Graph is not indicative to guaranteed rate of return. This graph is purely for illustration purposes and is subject to change based on market conditions and investment strategy.

This doesn’t replace other planning — it complements it

For most families, priorities still apply: emergency reserves first, then retirement savings, then education planning, then additional long-term tools like this one. A Trump Account used in isolation misses the point. The real value comes from coordination and knowing how it sits alongside a 529, a Roth IRA, and a taxable account, and letting each piece do what it does best.

No single account creates generational wealth. What does is the intentional coordination of time, tax strategy, and structure that is started earlier than feels necessary, and revisited as life changes. That’s the kind of planning that compounds the same way the money does.

Is this worth your family’s attention?

If you have a child born between 2025 and 2028, the $1,000 alone makes this worth opening. But the window to plan around the conversion opportunity is shorter than it seems and the decisions you make early are the ones that are hardest to undo later.

How this fits into your family’s broader financial picture depends entirely on your tax situation, timeline, and goals. That’s the conversation worth having before July.

If you’d like to think through what this looks like for your family specifically, Book a time by following the link below

https://calendly.com/vilas-preparedretirementinstitute/gettingtoknowyou

The best time to plan around a compounding asset is before the compounding starts.