Insurance: The Part of Your Financial Plan You Hope You’ll Never Need

How thoughtful risk management helps protect the nest egg you’ve built when life doesn’t go according to plan.

When people think about financial planning, they often focus on the tangible aspects of the process: investment performance, retirement projections, tax strategies, and wealth accumulation. These are all important components of a successful plan, but they share one underlying assumption: the plan has the opportunity to work as intended.

Financial plans can be disrupted by more than just market volatility. More often, disruptions occur because of life itself: home repairs, auto accidents, an injury or illness during peak earning years, the loss of income, a long-term care event, or a spouse forced to navigate complex financial decisions while grieving. While insurance cannot eliminate those hardships, it can help reduce the financial strain that often accompanies them.

Unlike investment performance, which is visible through statements and market updates, the value of insurance isn’t quantifiable until it is needed. Yet its role can be just as important to a successful plan - helping protect the financial life clients spend years, even decades, building.

Mistakenly, insurance is often viewed as a passive standalone product. A policy is purchased; the premiums are paid faithfully, yet the same coverage remains in place for years.

The reality is that the circumstances surrounding that coverage rarely remain unchanged. Financial plans evolve over time and coverage that was once appropriate may no longer reflect a person's current needs and goals. An important question to revisit regularly is: does this coverage still align with the life it is intended to protect?

As wealth grows and financial lives become more complex, risks emerge beyond life and disability coverage that can affect the broader financial plan. Property, liability, and additional forms of protection become increasingly important, not simply to insure individual assets, but to help safeguard the financial foundation those assets support.

What Happens When Life Doesn't Go According to Plan?

One of the most valuable aspects of comprehensive planning is the ability to evaluate those risks before they become reality. Most financial plans appear strong under ideal assumptions. The true value of planning emerges when those assumptions are challenged.

Scenario analysis can help evaluate how a financial plan responds when key assumptions change. By modeling alternative outcomes, it becomes possible to better understand the potential impact of various risks, identify areas where additional protection may be beneficial, and uncover opportunities to strengthen the overall plan. Those insights often lead to some of the most meaningful planning conversations.

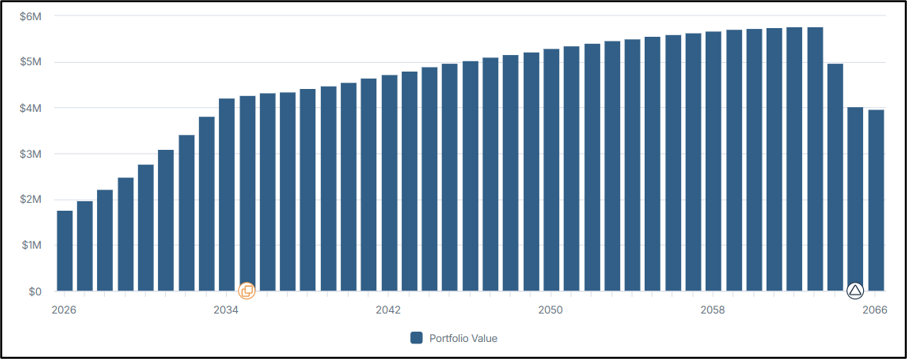

Consider a hypothetical couple in their late 50s who are planning to retire within the next decade. Their children are financially independent, they have accumulated meaningful retirement assets, and they continue to make progress toward paying their mortgage. They both carry $500,000 term life insurance policies. Under normal assumptions, their retirement projections remain on track.

Base Plan Lifetime Portfolio Value

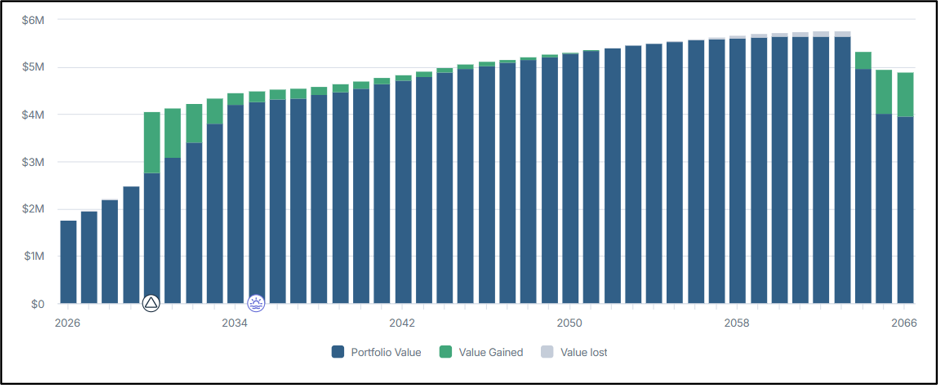

As part of the PRI planning process, we model a scenario where one spouse passes unexpectedly before retirement. While the surviving spouse would receive life insurance death benefits and inherit the family's assets, the loss of future earnings creates a meaningful shift in the long-term outlook.

Alternative Scenario: Lifetime Portfolio Value if Client unexpectedly passes at age 60 with their current $500k life insurance policy

We further evaluate how different levels of protection affect the outcome. In this example, an additional $750,000 of life insurance meaningfully improves the projected results, particularly during the years leading up to the surviving spouse's retirement. The additional proceeds help replace lost income, reduce pressure on investment assets, and provide greater flexibility during a period when the surviving spouse may be navigating both emotional and financial challenges.

Scenario: Client unexpectedly passes away at age 60 with and additional $750k life insurance policy

The value of financial modeling lies in identifying potential vulnerabilities before they become reality. By understanding how a major life event could affect the family's financial future, planning decisions can be made proactively rather than reactively.

A Final Thought: Building Resilience into the Plan

At Prepared Retirement Institute, we believe the most effective planning balances both opportunity and protection. Our planning approach focuses on helping clients protect what they have built, prepare for life's uncertainties, and make informed decisions as circumstances evolve.

By evaluating insurance through the lens of comprehensive planning and scenario analysis, it becomes possible to understand how risks may affect long-term goals. This planning-first approach helps move the conversation beyond simply focusing on insurance coverage alone and toward a more meaningful question: "Is my financial plan resilient if life doesn't unfold as expected?"

In some cases, the analysis confirms that existing protections are sufficient. In others, it may reveal opportunities to strengthen the plan or address risks that had previously gone unnoticed. Either outcome provides valuable clarity.

If you've experienced a major life change, accumulated significant assets, or simply haven't reviewed your coverage in recent years, our team can evaluate whether the financial life you've worked hard to build is protected across a range of possible outcomes.

Graphs are for illustrative purposes only and were generated using financial planning software. Please contact your financial advisor for more information based on your individual circumstances.